Getting a life insurance policy is one of those adulting things that we all need to take care of at some point or another. Life insurance is a valuable way to protect the financial future of yourself and your loved ones.

In fact, 64% of Canadians put the most value on life insurance when compared to other insurance products. They understand that investing in these policies is a way to plan for the future and protect your loved ones.

If life insurance is something that has been mulling around your mind recently, the easiest way to get started is with Insurdinary's Life Quoter. Here's everything you need to know about this tool.

Disclaimer: All, or some of the products featured on this page are from our affiliated partners who may compensate us for actions and or sales completed as a result of the user navigating the links or images within the content. How we present the information may be influenced by that, but it in no way impacts the quality and accuracy of the research we have conducted at the time we published the article. Users may choose to visit the actual company website for more information.

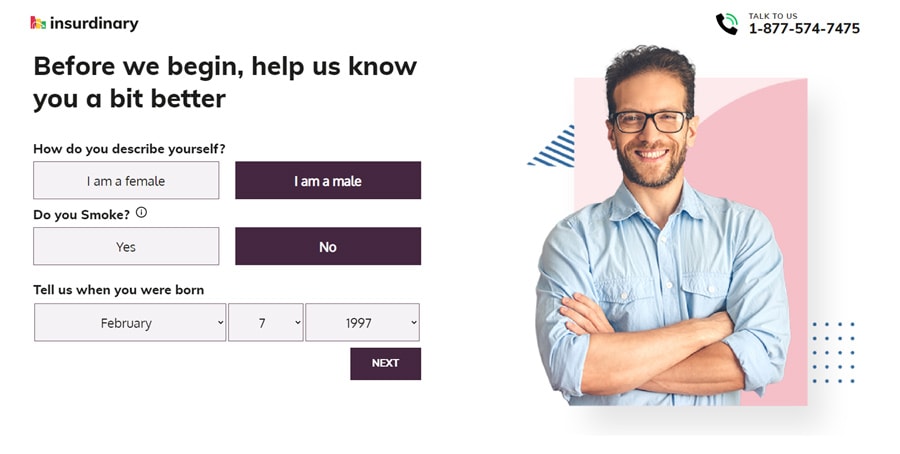

The first step to getting a life insurance policy quote is to fill out your basic information. When you head to the quoter, you'll be asked for some vital details. Let's take a look at what basic info is needed to take out a policy.

Gender

The first question on the quoter is your gender identity. At the moment the quoter asks you to select whether you identify as male or female.

The reason for this is that underwriters still only use male and female genders in their process. At the moment actuaries don't have enough information to include other genders, and so it will ask people to select either male or female.

The difference in premium rates for men and women is due to their mortality rates. Insurance rates are almost always less expensive than men for two very simple reasons: women are considered low risk and women live longer than men.

Do You Smoke?

Another piece of basic information that you'll be asked is whether or not you smoke. Insurance premiums are based on how likely the insurer is to payout, which is affected by smoking.

Smokers are at an increased risk of dying young. What that means is that life insurance for smokers is usually quite a bit higher than it is for non-smokers since companies are more likely to payout.

Date of Birth

The third major piece of information you'll be asked to input is your date of birth. This also helps insurers determine your rate also.

In general, life insurance premiums increase each year you age. It can be as low as 5% a year or as high as 12% a year depending on how young or old you are. This is why it is wise to secure a life insurance policy when you are young and healthy.

Your age will also determine what type of policy you qualify for. Some companies will offer different terms for people of different ages.

And, your age can also determine whether or not additional requirements are needed for your policy. Health insurance providers may, for example, request health tests for older adults seeking to take out a life insurance policy.

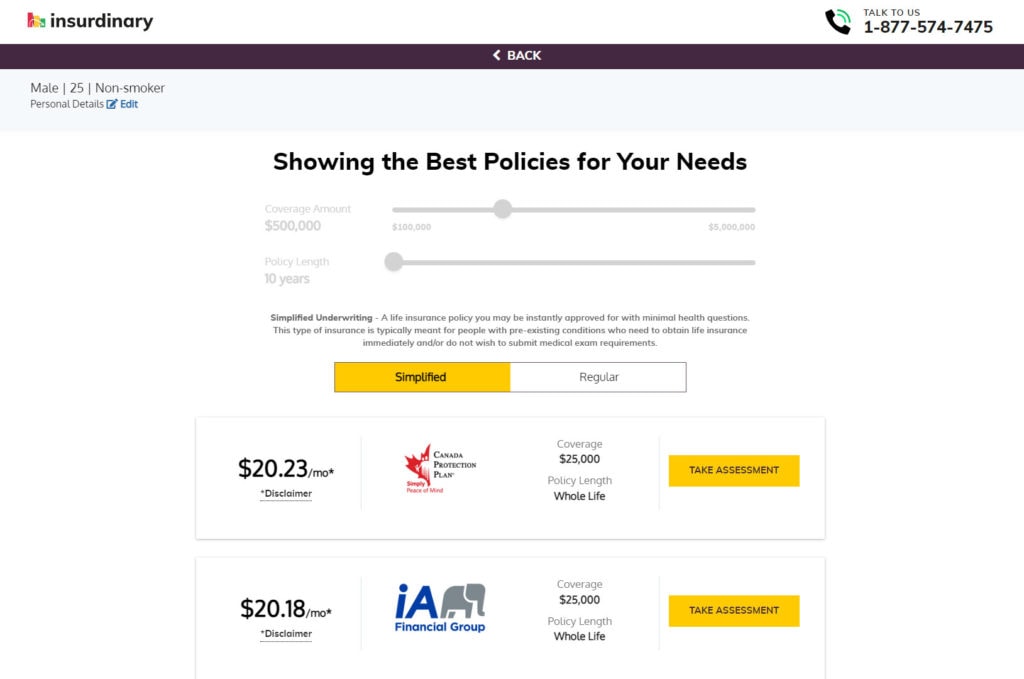

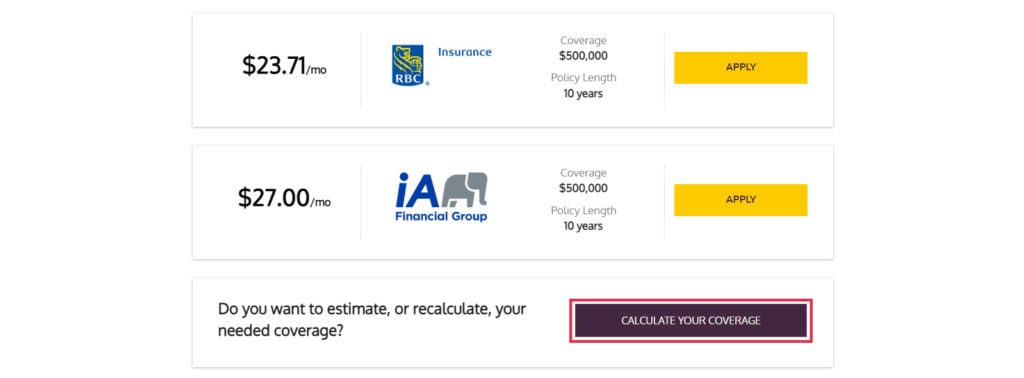

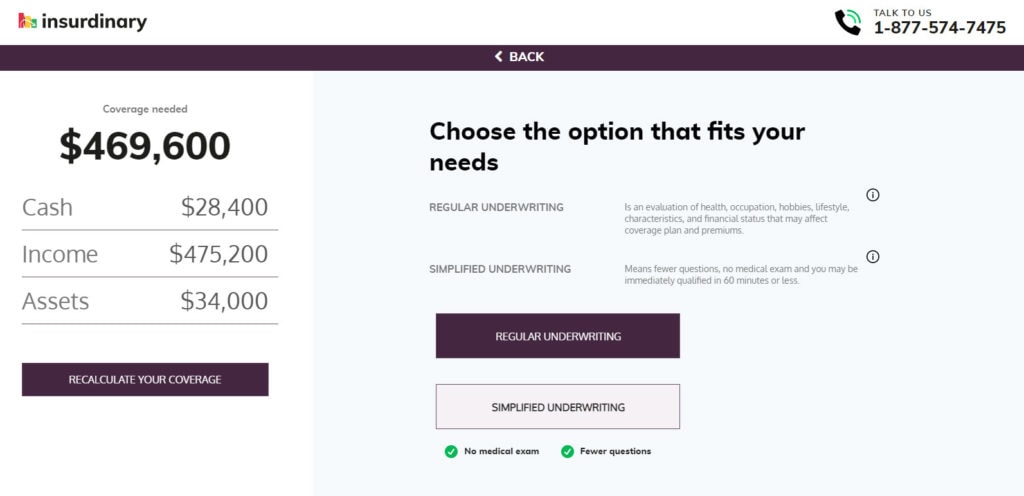

Once you've plugged in all your basic information, you'll be taken to a page that helps you choose an available insurance policy. By default, you will be shown plans for simplified underwriting. You have the option to view regular or simplified policy plans using the selector.

On Choosing a Simplified Policy

Simplified underwriting is a life insurance policy you may be instantly approved for with minimal health questions. This type of insurance is typically meant for people with pre-existing conditions who need to obtain life insurance immediately and may, or may not, wish to submit medical exam requirements.

A rate for a Whole Life plan may be shown immediately before taking an assessment, based on the applicant's basic information. This is only a preview of a sample rate with a default coverage of $25,000. This rate is available to be applied for if the applicant completes the assessment - answering "No" to all questions. The applicant will still be able to change the coverage amount and term length, if those options are available.

Assessment Steps

To apply for a simplified life insurance policy, you'll first have to take an assessment to see if you're eligible for this type of life insurance. The questionnaires on the assessment are:

Are you unable to independently complete at least 2 daily life activities?

Do you reside in a long-term care facility?

Do you need an organ transplant?

Have you spent more than 48 hours in a hospital in the last 30 days?

Have you received abnormal tests or surgeries in the last 60 days?

Do you have a terminal condition with 24 months or less to live?

Have you ever been diagnosed with HIV or AIDS?

Have you ever had a treatment for a life-threatening disease?

Have you received treatment for a life-threatening issue prior to age 40?

Have you used any type of drug in the past 12 months?

Have you been incarcerated or convicted of a crime in the last 12 months?

Are you considered overweight for your age?

These questionnaires screen individuals for their eligibility for a life insurance policy. There are four sections on the assessment which determine your eligibility for different life insurance policy amounts. Individuals who meet a certain number of these criteria may not be able to take advantage of the simplified underwriting process. Answering "Yes" to some of these questions could affect the maximum amount you'll be able to take out in a policy.

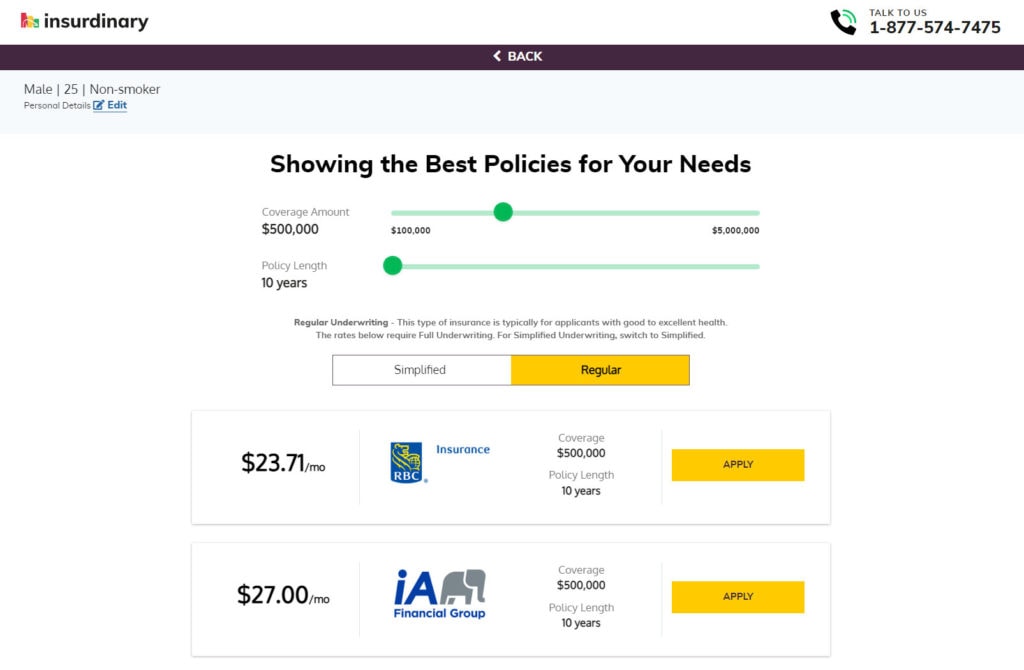

When you qualify for a plan, you will be able to view the rate for that insurance product. Upon viewing your rate, you will be shown the monthly premium for that product. Like with the regular policy plans, you will now be able to change the desired coverage amount and term length with sliders. Note that certain plans have limited minimum and maximum coverage and may not offer certain terms.

Regular underwriting is a type of insurance that‘s typically for applicants with good to excellent health. As such, the plans for them require full underwriting.

There are two sliders you can use to customize the regular policy plans provided. The first slider will allow you to change your needed coverage amount. The second slider will allow you to change the length of the term.

If you want to apply for any of the available plans, select the “Apply” button to the right of the desired plan. Afterwards, you will be able to start filling out the following information for your insurance application.

After Selecting a Plan

When applying for either simplified or regular underwriting plans, they both follow the same procedure. After completing all the following steps, you will be able to review and complete your application.

Questionnaire 1: Full Detailed Information

If after taking the assessment you get approval for simplified life insurance policies, you'll be able to complete the application process. The first part of the process will require you to provide detailed personal information. The key information you entered in this form will be evaluated by the company providing the insurance plan. Depending on the company and the policy selected, the questions needed to be answered will vary. The required information may include, more or less of, the following:

Your full name

Your address

Social Insurance Number (for whole life policies)

Other pending insurance applications

Whether or not you've been declined for insurance

If you have in-force insurance (apart from credit or group insurance)

Your last tobacco usage

Whether you were born in Canada or not

Your completed level of education

Your occupation

Your ID

Who will pay for the policy

Whether an applicant is a Canadian citizen or resident

Whether an applicant resides in a foreign tax jurisdiction

These details are important for placing the policy under your name. It's also important for determining eligibility, coverage amounts and tax information. Some of that information such as your education level and occupation can also be used to get you lower rates.

Questionnaire 2: Beneficiary Information

After you've filled out your information, you'll be taken to a page for adding beneficiaries. The information needed for each beneficiary includes:

Beneficiary first and last name

Relationship to Insured

Date of birth

Share percentage

Beneficiary type

Whether the beneficiary is primary or contingent

Beneficiary gender

Life insurance providers need this beneficiary/ies details so that they know who to pay in the event that you pass away. You can add multiple beneficiaries if you want to split the payout between more than one person.

If you do add additional beneficiaries, you'll be able to select the percentage of the payout they receive. That way, you can divide your life insurance policy up however you best see fit.

Questionnaire 3: Banking Information

Finally, you'll be required to input your banking information. This information is important because it is what you'll use to pay for your policy.

As part of your details, you'll be able to select whether you'd like to pay your premium monthly or annually. You'll also be able to set up a pre-authorized debit if you would like. Pre-authorized debit services withdraw the money from your account automatically. That way, you don't have to worry about remembering to make your payments on time.

As part of your agreement, you'll have to provide contact details. This helps the bank follow up with you in the event that there are any issues debiting your life insurance premium.

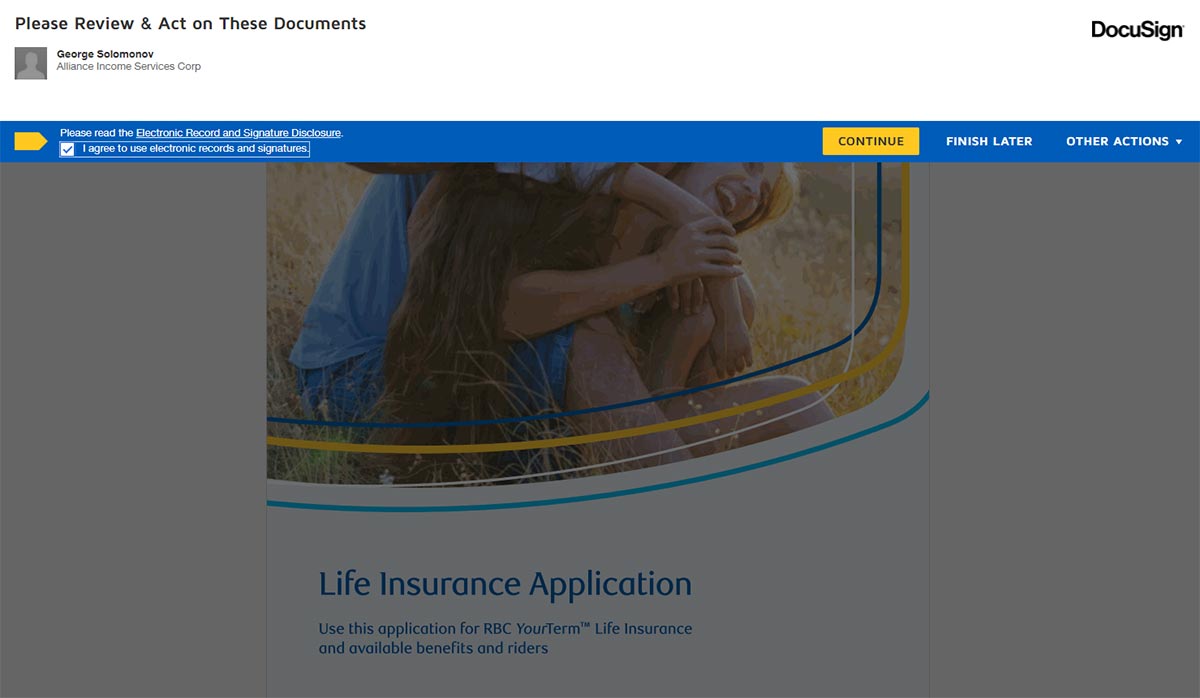

Step 3: Complete Your Application Using DocuSign

Once you've successfully completed your application on the quoter, your application will be reviewed and you will receive a confirmation email. You might be contacted for any medical requirements that the Insurer may need. After the review process, an email with the life insurance form with the information filled out, including the premium amount, will be sent to you - requesting your electronic signature via DocuSign.

DocuSign is a platform that allows you to upload and sign official documents. It's a way of storing and signing papers digitally so that you don't have to deal with printing out mounds of papers and scanning them back into the computer.

After you've reviewed your application, you can start clicking on the fields that prompt for a signature. Once you've finished signing, complete the application on the upper right of the page and your application will be sent to the Insurer.

I Need Help: Recommendation on My Coverage Amount

If you are unsure about how much coverage you need, you can get a quick calculation based on your cash needs, income replacement and assets.

Cash Needs Section

The cash needs section requests five different pieces of information:

Final expenses

Mortgage

Other loans

Children's education fund

Emergency fund

You'll need to input the applicable amounts to each section. The quoter provides you with some information on what standard amounts for each of the five requirements are to help you out.

Your cash needs are important in helping you determine how much life insurance you really need. The more cash you'll need, the larger the life insurance policy you might want to take out.

Income Replacement Section

The next section is the income replacement section. This section of the form asks you just two simple questions:

Monthly income requirements to care for your family

Number of years of support you're looking for

This section is important for helping determine how long of a life insurance policy you need as well as what monthly payout you need to care for your loved ones.

The more time you'll need support, the longer a life insurance policy you'll need. Plus, the more monthly income you require to care for your family, the higher the policy amount you'll want to take out.

Assets Section

The last section asks you to fill out three key pieces of information:

Your current savings

Other assets

Existing life insurance policies

This information is helpful for lowering your rates. If you already have a good amount of savings and other assets, these can be liquefied and used to help support your family after your death.

Similarly, if you have existing life insurance policies already, those can be used to care for your family after you are gone. Having additional policies means you don't need as much coverage from a new policy.

After receiving your estimate, you'll have an idea on how much coverage you need before applying for a plan. If you feel that you've made a mistake in any of the three calculation steps, you can navigate back using the Back button at the top or using the "Recalculate Your Coverage" button.

How Different Scenarios Yield Different Results

Every individual has a unique scenario. And, the results of your personal scenario will affect the results that you receive.

To get a better understanding of how different scenarios yield different results, let's take a look at a few scenarios. Here are three different situations where individuals receive life insurance quotes. Please note that these rates were accurate at the time the article was written and could have been subject to change.

Scenario #1

Our first scenario is looking at a non-smoking, 25-year-old female who lives at home and has no expenses. Let's say that this person is looking for a $100,000 plan.

A young woman in this scenario will be offered policies which will vary depending on what term she chooses:

Insurance Quotation Option

No. of Years

Amount

1

10

$9.00 - $9.27 per Month

2

15

$10.08 per Month

3

20

$10.08 - $10.98 per Month

4

25

$11.75 - $11.79 per Month

5

30

$12.60 per Month

6

Whole Life

$50.85 - $99.34 per Month

In addition, she'll be able to choose between two different providers:

iA Financial Group

RBC Insurance

Keep in mind that not all providers offer all the aforementioned policies.

Scenario #2

Let's take a look at a slightly different scenario. In this case, let's look at quotes for a 42-year-old woman who is a smoker, has $10,000 left on her mortgage, $5,000 in car loans, and $7,000 on her credit cards.

Imagine that this woman is in need of a 1-million-dollar plan. Her policy rates will vary depending on the term she selects:

Insurance Quotation Option

No. of Years

Amount

1

10

$124.20 - $128.34 per Month

2

15

$179.10 - $184.32 per Month

3

20

$216.00 - $234.09 per Month

4

25

$281.70 - $296.73 per Month

5

30

$355.50 - $376.47 per Month

6

Whole Life

$1181.70 - $1,800.63 per Month

Scenario #3

In our last scenario, let's take a look at a 50-year-old man, who is a non-smoker, who has $60,000 worth of debt and $10,000 worth of savings. Let's say that he's looking for a $500,000 plan.

The regular policy rates a man in this position would see available are as follows:

Insurance Quotation Option

No. of Years

Amount

1

10

$62.59 - $67.95 per Month

2

15

$98.32 - $102.60 per Month

3

20

$123.93 - $127.80 per Month

4

25

$172.26 - $183.15 per Month

5

30

$239.31 - $274.50 per Month

6

Whole Life

$711.45 - $1098.90 per Month

This gentleman would have access to two different lenders:

iA Financial Group

RBC Insurance

Once again, the rates that this man receives are very different from those of the women in scenario #1 and scenario #2. His debt, age, and gender all played a role in what his coverage looks like.

It Really Doesn't Get Much Easier Than This!

Whether you know the coverage amount you require, or need some help with the calculations, we've got you covered.

Our amazing life insurance quoter isn't the only benefit of taking out a policy from Insurdinary. There are tons of reasons why Canadians choose to become clients with us.

Whether you're on the fence about your quote or you just want to learn more, we've got some details for you. Let's take a look at some of the top reasons why customers become clients at Insurdinary.

Our Excellent Reviews

We've got tons of great reviews from clients, showing how we've helped others in the past. Clients have tons to say about their experience working with us and how it's helped them get a great insurance policy.

For one, clients talk about our honesty. All costs and fees are clear and upfront, all the time. Our team cares about providing you with accurate and transparent quotes, which is one of the reasons we've received such positive reviews.

On top of that, we love what we do. Clients note that the passion we have for our insurance products shows through in our work. Since we care about what we do, we care about our clients, which is one of the reasons we've gained such positive feedback from them.

Our Stellar Customer Service Team

It's not just our reviews that speak for themselves. It's also our customer service team and our commitment to our customers.

Our customer service team never oversells. We want to get you life insurance policies that actually make sense for your needs, rather than just close a deal.

On top of that, our customer service team gets back to you fast. If you have an issue, question, or concern, you know that you'll hear back from your representative in just a few hours with an answer!

Finally, we listen. When our customers reach out to us, we take the time to fully listen to their requests. That way we can address their queries in the best possible manner.

Our Attention to Detail

Another major reason why so many clients love working with Insurdinary is because of our attention to detail. Our team carefully analyzes every part of your application to make sure there's nothing missing.

You'll never find our representative skimming over tasks or hurrying to get the job done. Instead, we hone in and focus on every detail of your policy so that we can make sure we really are getting you a great quote.

By paying attention to detail, we're able to catch things that other companies wouldn't. That means bigger savings for you and better life insurance policies overall.

Prefer to Speak to an Advisor? We Can Do That Too

We are proud of our life quoter. It's a great tool for learning what your benefits and payouts will be when you invest in a life insurance policy.

If you've still got questions, however, speaking to an advisor might be beneficial if you prefer a human touch. Get in touch with our team today. We are looking forward to answering all of your questions.

Important Notice:

All interest rates, fees, and other numerical figures displayed on our website are subject to change without prior notice. To ensure you have the most current information and/or promotion, please visit the provider's official website.