The idea of putting a foot forward and purchasing a home might be kind of a scary one. To add to the stress of the process, buying a house during COVID 19 certainly adds a couple of things that you have to consider as you start to plan.

For one, how are the markets doing after the global economic difficulty? Can we expect them to get even worse? What does that mean for me if I'm buying a home?

Those questions sit on top of the other general questions and concerns that you might be having as someone investing in a property. We're going to take a look at some of the considerations you should make if you're looking to buy or sell a home right now.

Disclaimer: All, or some of the products featured on this page are from our affiliated partners who may compensate us for actions and or sales completed as a result of the user navigating the links or images within the content. How we present the information may be influenced by that, but it in no way impacts the quality and accuracy of the research we have conducted at the time we published the article. Users may choose to visit the actual company website for more information.

Selling or Buying a House During COVID 19: Is It a Good Time?

We'll split this discussion up into two primary pieces. First, we'll take a look at the main personal considerations and factors that you should be mulling over. At the end of the day, your personal situation is the best indicator as to whether or not you should be buying or selling a home right now. After that, we'll talk a little bit about the market conditions.

Am I Ready to Purchase a Home?

If you're thinking about buying a home, it's easy to just jump on that idea and ride it out, potentially making a few pitfalls along the way. If you take some time to examine your financial situation, though, you might be able to plan a little more carefully and wind up with a much better mortgage.

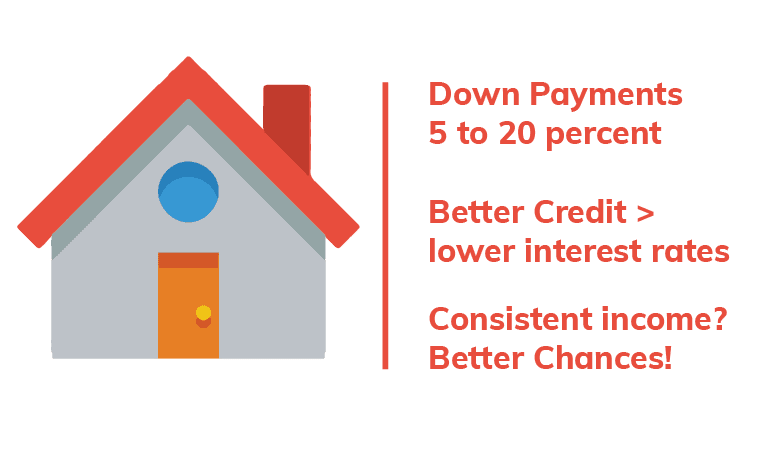

First, think about the amount of money you can reasonably put down for a down payment. The value you need to pay for the entire home will influence how much you should give for the down payment. In a lot of cases, the lender will require that you put a specific percentage forward, typically anywhere from 5 to 20 percent, depending on your financial indicators. If you're a first-time buyer, some lenders will incentivize you to buy a home by only requiring you to put roughly 5 percent down. Though, the more you can muster up in terms of the down payment, the lower your interest payments will be.

Another thing to consider is the state of your credit score. Individuals with great credit scores usually get mortgages with lower interest rates. It's possible to improve your credit score within a year or two through the use of credit cards, paying bills on time, and lowering your debt to income ratio.

That brings us to the final main factor in whether you should be looking into buying a home. Have you had consistent income for the last two or three years? Lenders will look at that when they're considering whether or not to lend to you, or how good of rates they can offer you.

Taking a few years to earn a more consistent income history and boost your credit can help you save tens of thousands of dollars over the lifespan of your loan due to a lower interest rate.

If you would like to compare mortgage rates currently available to you, we suggest doing so through Breezeful, a digital mortgage broker. Breezeful allows you to compare rates from over 30 lenders and apply immediately online by uploading the necessary documents.

Breezeful - Online Mortgage Broker

Save thousands of dollars with rates others won't show you.

Selling a house is a big decision, and it's another one that can be easy to move forward with without too much planning. Once you get the idea to sell your home and move, you might be dead-set on carrying through with it regardless of the circumstances.

That said, there are some other considerations to take into account that could help you wind up with a better deal. First off, what is the reason that you want to move?

Is there a home that you've found which you think would be a better fit, or is it just a matter of wanting to get out of the place you're currently in? Furthermore, what are you looking at in terms of appreciation and equity on the home?

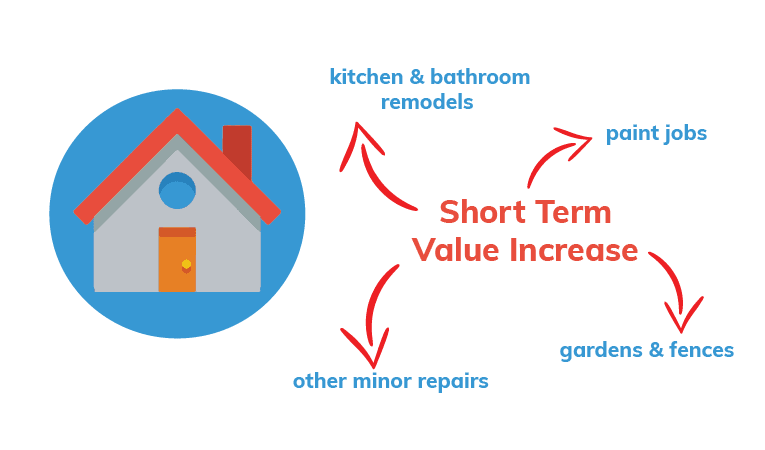

If at all possible, it's always best to see if there's a short-term way that you can increase the value of your home's appraisal before you sell it. In many cases, there are tons of things that you can do to boost the value significantly. For example, kitchen and bathroom remodels are investments that tend to fetch more than 150% return on every dollar you spend.

Similarly, small adjustments like paint jobs, gardens, fences, and other minor repairs can all add together to create a lot more value for your home.

If your reason for wanting to move is that you need money or are struggling as a result of the pandemic, it might be a great time to work on those small remodels and consider refinancing your home. When you refinance at a time when the market is doing well, you can get the appreciated value of your home in-hand and use that cash to pay for other pressing issues in your life.

How is The Canadian Housing Market Doing Right Now?

Canada suffered a little bit early on during the pandemic, but things have recovered and remained relatively steady throughout the last leg of 2020 and into 2021.

In fact, average market prices are expected to rise by 4 to 6 percent in Canada, according to RE/MAX. It seems that individuals who are investing in more expensive homes, as well as individuals who are moving into Canada from abroad, are contributing to this sustained health in the market.

Additionally, individuals are increasingly looking to move out of densely-populated cities and into smaller towns with more land per-capita. Canada is a great place to do this, so there's a lot of internal shifting within the country, and also many United States residents are making the short hike north.

Factors Driving Up Canadian Home Values

There's something to be said about the way that the Canadian government handled the pandemic in terms of financial relief as well as health care treatment.

From the $2,000 checks each month to the fact that access to medical care is relatively smooth for most people, there may have been less of an economic downturn as a result.

Those checks may have even prompted some individuals to make renovations to their homes and add value. Tack these factors onto the natural growth of home values, and you've got a Canadian market that is ripe for buying and selling.

Let's take a look at whether or not you should be buying or selling at this very moment, though.

Should I Buy a Home Right Now?

It appears that, if you're financially able to invest in a home, right now is a great time to do it as the markets are still recovering slightly from the effects of the pandemic.

The home value should only increase on average from here on out. That means a couple of things. First, it means that purchasing a home sooner than later will get you a lower price overall, and that means lower interest accruement and payments over the life of your loan.

Second, the investment in your home will start growing sooner and prosper more over time, barring another unforeseen economic collapse.

Therefore, looking into getting a loan on a house is a good idea right now considering the various factors of the Canadian housing market. What matters at this point, then, is whether you can find a lender that will provide you with a loan that works well for you.

How About Selling a Home?

In terms of selling, it might be a good idea to wait a little while as the market works to get back on its feet. Projections are varied in terms of how the market should fare going into the future, but most of them suggest a boom as the economy reacquaints itself with the normal way of things.

It's always a gamble to sell a home, though. You could sell your home and find that value skyrockets in the following years and you could have made a great haul.

That said, you could wait that amount of time and see another economic collapse, only to have prices fall significantly and take decades to recover. It's a gamble.

If you're not sure about what to do, take a look at your personal situation and whether or not your house has accrued a lot of equity since you've purchased it.

Equity and Personal Situation

You might just really want to move out of the place you're living in currently. There's nothing wrong with that.

There's especially nothing wrong with that if you've accrued some value on your home and can use the money from the sale to buy a more valuable house. Investing in another property that you plan to live in for a long time might be the more practical move than waiting.

If you wait, you might not get back to the value that your home is currently at, whereas selling will put that money right into your hands. When you use that money to invest in a new home, you'll at least have the new property and you can weather the economic ups and downs in a place that you want to live in.

So, if you just simply want to find a new place, there's nothing wrong with swapping homes and waiting to see what the markets do someplace that you enjoy living in.

It's also important to note that the value of a more expensive home will rise significantly if the markets do well. That means that it might also be a wise financial choice to sell your home and buy a new one right now if you have the means.

What about Finding Lenders and Getting Good Rates?

As you start the process of figuring out which banks and lenders you're going to work with throughout your home buying and selling journey, you're going to need to narrow down some potential lenders.

Take a look at whatever options you can reasonably get approved for and start comparing them.

Having a wide range of options to consider can help you make the best decision and wind up with the best mortgage for you. Additionally, seeing how different options stack up and what the requirements are to qualify for those loans might give you some ideas on how to move forward.

For example, you might see that an excellent option is just out of reach for your income level and credit score. That could be an incentive to work hard for another year or two and improve your credit so that you can get a mortgage at a better rate in the future.

If you're having a hard time finding great lending options, you can explore our site for resources on some of the Canadian lenders with the best rates around.

Interested in Learning More?

Buying a house during COVID 19 is both exciting and scary. We're here to help you through it. Just because things are a little hectic out there doesn't mean that we can't take significant steps to improve our future.

If you're serious about purchasing a home, you will need mortgage insurance. Request a quote and compare rates and coverages!

Important Notice:

All interest rates, fees, and other numerical figures displayed on our website are subject to change without prior notice. To ensure you have the most current information and/or promotion, please visit the provider's official website.